The small business retirement wave is accelerating—and many communities are unprepared. Over the next decade, millions of U.S. small business owners will reach retirement age. The urgent question: What happens when the owner retires? According to new research from the McKinsey Global Institute, roughly six million owners will step away, representing trillions in enterprise value. Yet most of these businesses may never be sold. Instead, they risk shutting down—taking jobs, local services, and generational wealth with them.

Among the six million owners nearing retirement, about one million lead firms viable for sale. Together, these businesses represent up to $5 trillion in enterprise value. However, current trends suggest as many as 92% could close rather than transfer ownership. The issue isn’t always profitability. Many are simply too small for private equity and too complex for informal family handoffs. Without prepared buyers, viable companies quietly disappear.

This signals a structural market challenge, not a lack of opportunity. Institutional investors often target companies valued above $5 million, leaving micro and lower middle-market firms overlooked. Meanwhile, informal buyers struggle with financing and deal complexity. As the retirement wave grows, the ownership gap widens. Communities dependent on these firms face economic ripple effects.

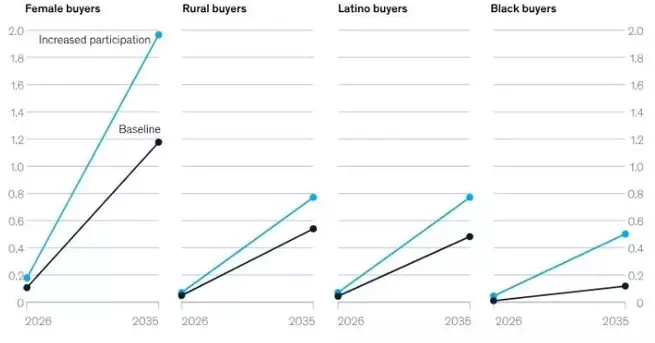

Business ownership in the United States is still concentrated among a narrow demographic. Under current patterns, only about 28% of the enterprise value expected to transfer will go to women and Black and Latino individuals combined. That imbalance limits the pool of successors. It also constrains wealth-building opportunities for underrepresented communities. Without broader access, the ownership pipeline cannot absorb the coming surge.

Small business acquisitions are often opaque and relationship-driven. Financing is fragmented, and transaction costs are high relative to firm size. Many potential buyers lack both capital and networks. As a result, viable firms close not because they fail—but because successors are scarce. Expanding access to ownership is increasingly an economic necessity.

New ownership models are emerging to address the small business retirement crisis. Employee stock ownership plans, known as ESOPs, allow workers to gain equity over time without large upfront investment. Seller-financed buyouts reduce immediate cash requirements and spread risk. Standardized lending products make smaller transactions more accessible to banks. Entrepreneurship-through-acquisition programs prepare first-time buyers to step into leadership roles.

These structures transform succession from a bespoke negotiation into a scalable process. By lowering barriers, they widen the ownership pool. They also preserve jobs and institutional knowledge. When succession is intentional, retirement becomes a transition—not a shutdown.

In Cornelius, Oregon, one business owner faced this dilemma directly. Grace Dinsdale, founder of Blooming Nursery, built her wholesale plant company over four decades. Without a clear buyer, more than 100 jobs—most held by Latino workers—were at risk. In 2023, she chose to sell the company to employees through an ESOP. Shares are now held in trust, allowing workers to build ownership stakes gradually.

This model preserved both livelihoods and legacy. It also created wealth-building potential for employees’ families. One worker’s daughter recently joined the firm, beginning her own path toward equity. The business continues to operate, not because retirement was avoided—but because succession was structured. The difference is profound.

The broader implications extend far beyond a single town. Research indicates that successful ownership transitions over the next decade could preserve up to 12 million jobs. That preservation depends less on injecting new capital and more on modernizing connections among buyers, sellers, and lenders. Without systemic change, communities may lose cornerstones of their local economies. With reform, they could unlock generational wealth transfer at scale.

Retirement is inevitable for small business owners. Closure does not have to be. The durability of America’s small business backbone depends on building a wider, stronger ownership pipeline. As the retirement wave grows, the choices made now will shape local economies for decades.

Copyright © 2026

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Comment